Discover the legal, financing, tax and residency rules every expat must understand before buying property in Panama City, plus how to protect yields and avoid ROP pitfall

For many North American and European investors, Panama represents the ultimate "Plan B." It offers a stable, dollarized economy, a skyline that rivals Miami, and a lifestyle that feels like permanent vacation. However, the amateur mistake I see most often is treating the Panamanian market like a domestic one. In my years navigating this landscape, I’ve seen paradise turn into a legal purgatory because an investor didn't understand the "asterisk"—the technical machinery of Panamanian law that separates a dream asset from a costly liability.

Success here requires looking past the glossy brochures. It demands the discipline of a legal navigator who prioritizes Public Registry data over a developer’s promises. If you want to secure a high-yield haven, you must understand these five strategic realities.

The Beachfront Mirage: Titled Land vs. Right of Possession (ROP)

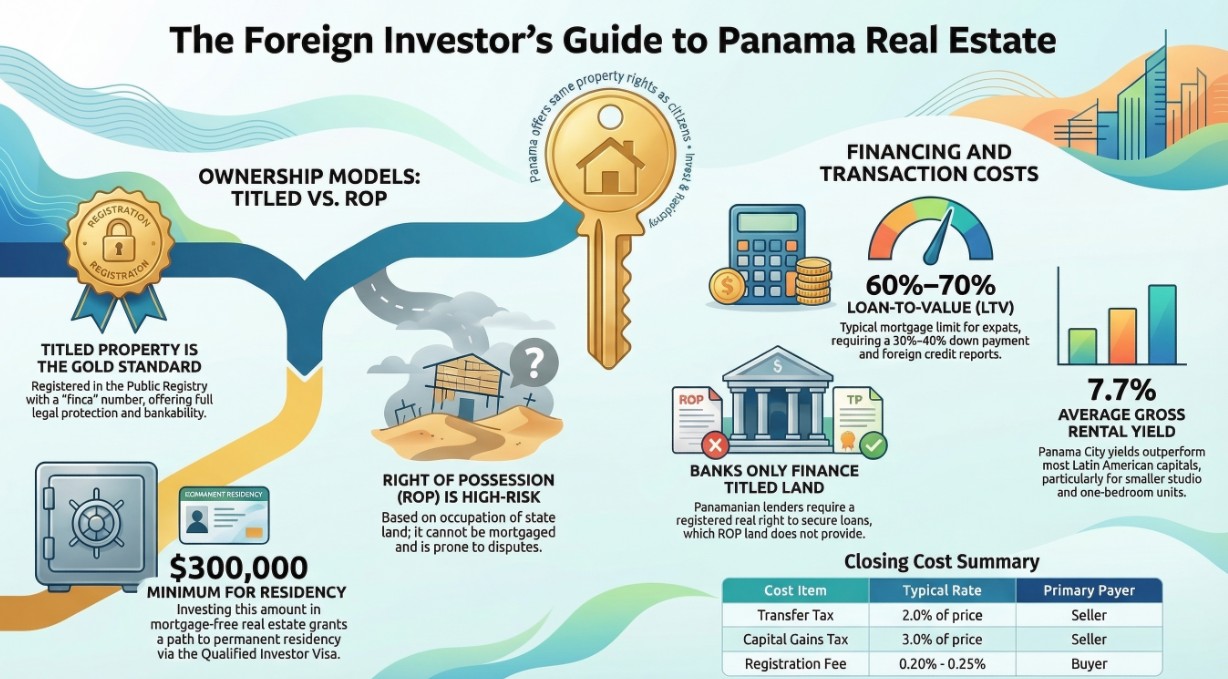

The most dangerous pitfall in the Panamanian market is failing to distinguish between Propiedad Titulada (Titled Property) and Derecho Posesorio (Right of Possession or ROP). Titled property is registered in the Registro Público de Panamá and assigned a unique finca (folio) number. This is the gold standard; it provides clear priority, strong legal protection, and is the only property type a bank will mortgage.

In contrast, ROP land is technically owned by the State. Your "ownership" is merely a recognized right of occupation. Most beachfront and island properties offered to expats fall into this category. The risks are profound: boundaries are often based on "the old fence" rather than coordinates, and your claim can be challenged by rival possessors or government reclassification.

"Most Panama beachfront offered to foreigners is not fully titled land but 'Derecho Posesorio' (Right of Possession), which has much weaker legal protection and far higher litigation risk." — Lawzana

As an expert strategist, my advice is firm: unless you are a seasoned developer with a three-year timeline and deep local legal roots to navigate the ANATI titling process, buy titled land. In Panama, title insurance is not standard because the Public Registry is the insurance. Due diligence must start with a certificación registral to verify the finca number and ensure there are no hidden liens or overlapping claims.

The "Size Matters" Yield Strategy: Why Small Units Win in Panama City

Panama City’s gross rental yields average approximately 7.7%, significantly outperforming regional peers like Mexico City or Bogota. However, I often see investors sink capital into luxury three-bedroom units only to see their yields stall below 7%. The data is clear: smaller units (studios and 1-BRs) are the engine of this market, delivering 8-10% gross yields.

The "why" comes down to the tenant pool. Panama City is a service-economy hub; smaller units attract a deep, consistent pool of young professionals and corporate expats who prioritize location and walkability over square footage. This translates directly to vacancy rates: well-priced small units see vacancies of 4-6%, while larger luxury units often sit empty for 10-15% of the year.

"The gap between gross and net yield in Panama City averages about 2.6 percentage points, meaning investors should expect to lose roughly one-third of their gross return to operating costs." — TheLatinvestor

To protect your net yield, you must budget for the "tropical maintenance factor"—specifically the accelerated replacement cycle for air conditioning systems—and high HOA fees, which are the largest components of your carry cost.

The Financing Reality Check: The FECI Tax and Expat Terms

Panamanian banks are open to foreigners, but they are conservative lenders. While a local might get 90% financing, an expat should expect to bring 30-50% to the table as a down payment. Interest rates currently hover between 7% and 9%.

Crucially, you must understand the FECI tax. This is a 1.0% surcharge (Special Interest Compensation Fund) applied to non-primary residence loans and investment properties. If you are not a permanent resident using the home as your primary dwelling, this tax is baked into your rate. Furthermore, banks enforce an "age + term" limit; the loan must typically be fully amortized by the time you reach 70 or 75, which can drastically shorten the term for retirees.

The "Big Three" expat-friendly banks are:

- Banco General: Panama’s largest; strict underwriting but highly stable.

- Banistmo: Often slightly more flexible with international income profiles.

- Scotiabank: Familiar with North American credit reporting standards.

The Golden Ticket: The Mortgage-Free Residency Requirement

The Qualified Investor Visa (Executive Decree 722) is Panama’s premier "Golden Visa," offering permanent residency in as little as 30 business days. For an investment of $300,000, it is a strategic masterstroke for those seeking a "Plan B." However, there is a legal condition that catch many by surprise: for this specific visa, the property must be mortgage-free (free of liens).

You cannot leverage your way into this residency; the $300,000 must be "clean" equity registered in the investor’s name or a legal entity where they are the ultimate beneficiary.

"The Panama Investment Visa allows investors to gain permanent residency through verified investments that demonstrate long-term commitment to the country." — Global Residence Index

This visa is a direct route to permanent status, bypassing the temporary stages required by other programs, and only requires a visit to Panama once every two years to maintain.

Hidden Tax Benefits and the "Paz y Salvo" Reality

Panama’s Territorial Tax System is a major draw—you are only taxed on income earned within Panama’s borders. For property owners, the rates are remarkably friendly compared to North America, but you must know the specific brackets.

For a primary residence, the first $120,000 is exempt. However, for secondary or investment properties, the brackets are:

- $0 – $30,000: 0% (Exempt)

- $30,001 – $250,000: 0.6%

- $250,001 – $500,000: 0.8%

- Over $500,000: 1.0%

When it comes time to sell, Panama offers a strategic choice for Capital Gains. The seller can choose to pay 3% of the total sale price (as an advance) or 10% of the actual net profit. A savvy strategist will calculate both to see which minimizes the tax hit.

Before any property can transfer, the seller must produce "Paz y Salvo" certificates. These are mandatory "good standing" clearances from the tax authority, water authority, and HOA, proving no debts are attached to the asset. As a buyer, you should budget for a registration fee of approximately 0.20% to 0.25% of the property's value to finalize the inscription in the Public Registry.

Conclusion: The Disciplined Path to Paradise

Panama remains one of the most attractive high-yield havens in the world, but it is a market that rewards technical precision and punishes those who rely on "glossy brochures." The path to a successful investment involves independent legal counsel, a focus on titled land with a verified finca number, and an understanding of the carry costs unique to the tropics.

As you evaluate your next move, I leave you with this: Is your priority the immediate allure of a beachfront ROP deal, or the long-term legal security and bankability of a registered title? In Panama, the second choice is always the one that lets you sleep at night.

Written by

Under500K Team

Research and market insights for global property investors.