Discover how Schengen entry, fast-rising purchasing power, new infrastructure, and shifting taxes are reshaping Romania’s real estate market for 2025 investors.

1. Introduction: The Emerging Tiger of the CEE

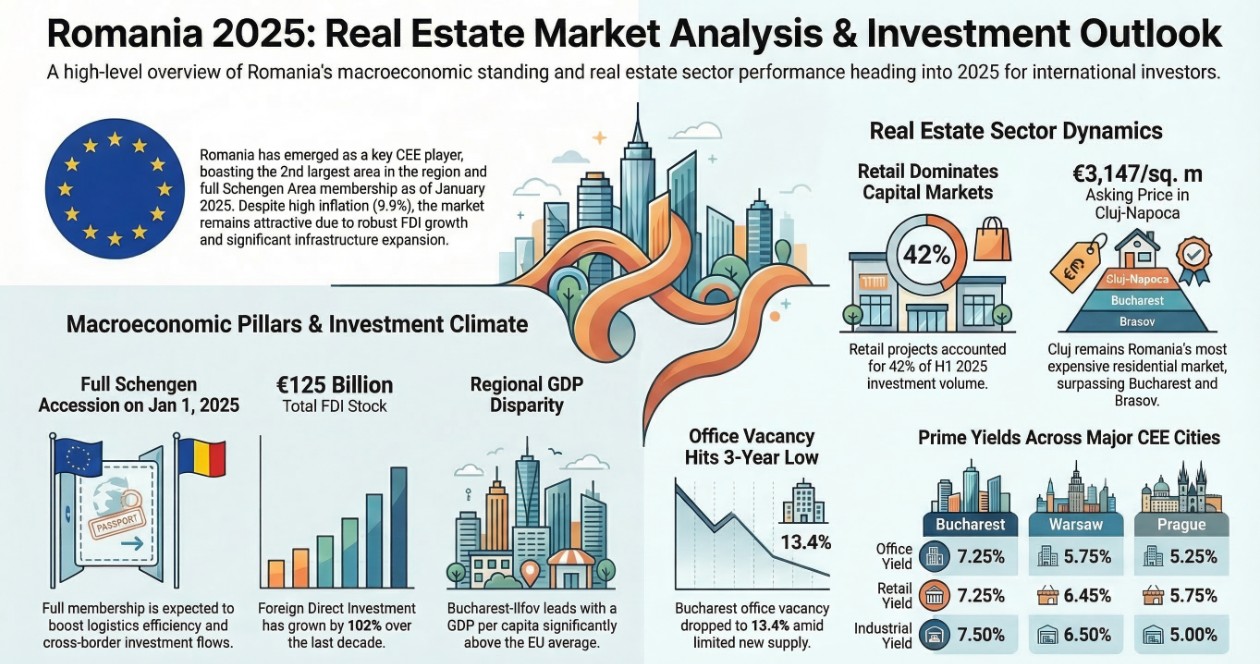

For decades, the global investment community viewed Romania through a sepia-toned lens—a landscape of post-communist transitions and industrial inertia. That perception was formally dismantled on January 1, 2025, when the country achieved full entry into the Schengen Area. Today, the "grey" stereotype has been replaced by a glass-and-steel reality in hubs like Bucharest and Cluj-Napoca. Romania has emerged as the CEE’s most compelling contradiction: it is a "Purchasing Power Paradox" where a daunting 9.9% inflation rate and a sluggish 0.6% GDP growth forecast for 2025 coexist with record-breaking Foreign Direct Investment (FDI) and a historic surge in household wealth. This is no longer a speculative frontier; it is a convergence market where sophisticated capital is betting on long-term structural tailwinds over short-term fiscal noise.

2. The Purchasing Power Paradox: Overtaking the Neighbors

The most visceral evidence of Romania's ascent is found in the Purchasing Power Standard (PPS). In 2011, Romania’s GDP per capita in PPS terms was a mere 52% of the EU average. By 2024, it reached 79%, a trajectory of convergence that has seen the country outpace the Euro Zone’s own growth (a 2.8% CAGR for Romania vs. 1.1% for the Euro Zone). This statistical "overtaking" is now a geopolitical reality, as Romania has surpassed the purchasing power of established peers including Hungary, Croatia, Greece, and Slovakia.

Romania has benefitted from a strong economic growth in the last decade, significantly reducing the gap in relation with the European Union average (especially after joining NATO and the EU in 2004 and 2007 respectively).

This is not merely a "catch-up" story; it is a fundamental realignment of the European economic map. For the strategist, the takeaway is clear: the local market has transformed from a low-cost labor pool into a robust consumer engine that is now wealthier than many of its regional neighbors.

3. The Residential Flip: Why Bucharest Isn't the Price Leader

In a defiance of standard urban economics, Romania’s capital is not its most expensive residential market. That title belongs to Cluj-Napoca, the "Silicon Valley of Transylvania." Despite Bucharest’s superior purchasing power—with an average net monthly salary of €1,462 compared to the national average of €1,049—it remains significantly more affordable than its Transylvanian rival. Bucharest’s asking prices are currently 33% lower than those in Cluj-Napoca, creating localized "price islands" driven by acute supply shortages and a high concentration of tech-sector wealth.

Top 3 Most Expensive Residential Markets (August 2025)

- Cluj-Napoca: €3,147 per net sq. m

- Brasov: €2,187 per net sq. m

- Bucharest: €2,102 per net sq. m

The "Cluj Effect" illustrates how specialized IT clusters can decouple local real estate from national averages. While Bucharest offers volume, the secondary cities are where the premium yields and supply-demand imbalances reside.

4. The Infrastructure Explosion: From 200km to 1,300km

Physical connectivity was once Romania’s "Achilles' heel," but a massive infrastructure mobilization is finally providing the backbone for its €125 billion FDI stock. In 2006, prior to EU accession, the country operated a negligible 228 km of highways. By August 2025, that network expanded to 1,329 km, with a further 724 km under construction and 683 km in the bidding phase. This expansion is complemented by an aviation surge, with 17 international airports processing 26 million passengers in 2024.

This physical connectivity is the primary driver behind the 102% increase in FDI since 2014. However, a strategist looks at the distribution: 65.4% of that FDI remains concentrated in the Bucharest-Ilfov region, while the North-East lags at just 2.3%. The ongoing highway projects targeting the North and East are not just engineering feats; they are the keys to unlocking the next wave of regional industrial growth.

5. Retail’s Unlikely Reign in a Digital Age

While global narratives suggest a retreat from physical retail, Romania’s institutional capital is moving in the opposite direction. In H1 2025, Retail captured the highest share of the investment market at 42%, comfortably surpassing the Office sector (32%). This trend is exemplified by M Core’s aggressive €150 million acquisition strategy, targeting retail parks in Focsani and Suceava alongside a series of regional strip malls.

Investors are prioritizing "risk-adjusted returns" and "yield stabilization" in an era of high interest rates (6.5% as of October 2025). In Romania, retail parks act as essential community hubs where e-commerce penetration remains secondary to the resilience of regional consumer demand.

The CEE investment market trajectory remains decidedly positive for the remainder of 2025, supported by yield stabilization, regional economic resilience, and the continued return of institutional capital.

6. The Fiscal Tightrope: VAT Hikes and Market Cooling

The momentum of 2025 faces a significant headwind in the form of aggressive fiscal reform. To bridge a persistent budget deficit, the government has implemented a series of tax escalations that have fundamentally altered the investment calculus. The most immediate impact has been in the residential sector, where the August 2025 VAT hike has significantly reduced housing sales and created sharp upward pressure on pricing.

The Velocity of Fiscal Change:

-

VAT Escalation: The standard rate rose from 19% to 21% in August 2025, marking the first change in eight years.

-

Dividend Tax Velocity: Rates have climbed from 8% to 10% in January 2025, with a confirmed jump to 16% scheduled for 2026.

-

Corporate and Turnover Taxes: While the 16% corporate rate remains stable, new turnover taxes for micro-enterprises (1% to 3% based on revenue thresholds) have added complexity for smaller operators.

These measures create a palpable tension between Romania's strong growth fundamentals and a "complex geo-political and fiscal climate" that demands a more cautious, data-heavy approach from developers and funds alike.

7. Conclusion: A Question of Momentum

Romania has successfully shed its "frontier" label to become a "convergence" market. The Schengen entry provided the psychological and logistical catalyst needed to solidify its status as a CEE powerhouse, yet the path forward requires walking a precarious fiscal tightrope. With interest rate cuts not expected until at least Q1 2026, the market is entering a phase where resilience will be tested by the very reforms meant to stabilize it.

The ultimate question for the next three years is one of gravitational pull: Is Romania the CEE’s new center of gravity, or is it merely flying too close to a fiscal sun? Owners of high-quality assets and those positioned in the "infrastructure-ready" regions of the West and Center will likely find the answer remains overwhelmingly positive.

Written by

Under500K Team

Research and market insights for global property investors.