Discover why Denmark’s cozy image hides lower net yields, strict foreign-buyer rules, and financing hurdles so you can avoid surprises before investing in 2026.

Denmark is frequently celebrated as the gold standard of European living, defined by a stable economy, pristine urban design, and the pervasive comfort of hygge. For the international investor or the expatriate looking to anchor themselves in Northern Europe, the Danish property market appears to be a harbor of safety. However, beneath the efficient facade lies a complex reality. The "Danish Dream" is not merely a transaction; it is a high-friction exercise in navigating a market that prioritizes social stability over speculative liquidity.

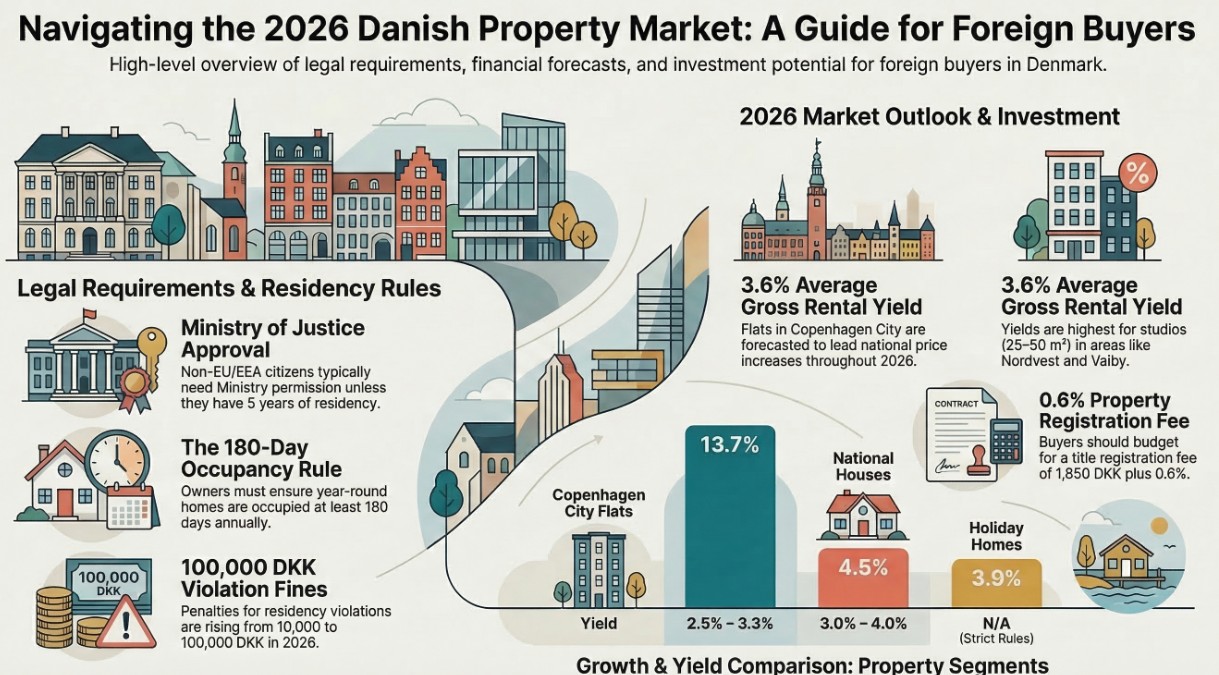

From the Ministry of Justice acting as an unexpected gatekeeper to the staggering fines for "ghost homes," here is what you need to know before signing a købsaftale (purchase agreement).

1. The Ministry of Justice is Your New Real Estate Agent

In most global capitals, the primary hurdles are financial. In Denmark, they are often ministerial. For non-EU/EEA citizens—and even for EU citizens who do not intend to use the property as a primary residence or to establish a business—explicit permission from the Ministry of Justice is a legal prerequisite. Unless you have resided in Denmark for at least five years or hold a permanent residence permit, you are essentially at the mercy of a bureaucrat's stamp.

This creates a brutal "speed trap" for foreign buyers. In hyper-competitive micro-markets like Frederiksberg or Indre By, where a desirable ejerlejlighed (owner-occupied flat) can sell within 48 hours, the week-long or month-long wait for Ministry approval is a deal-killer. You may have the capital, but without the residency permit or five years of history, you cannot move with the agility the market demands.

The consequences of ignoring this are absolute:

"If you buy property without meeting these requirements, the sale can be declared invalid, and you may be required to sell."

Buying without permission isn't just a fine; it’s a total loss of the asset.

2. The 100,000 Kroner "Empty House" Fine

Denmark is intensifying its war on property speculation through the aggressive enforcement of bopælspligt—the legal requirement that a year-round home must actually be occupied. Housing Minister Sophie Hæstorp Andersen has proposed a tenfold increase in penalties, moving from a negligible 10,000 DKK to a shocking 100,000 DKK fine for violations.

This isn't an empty threat. The municipality of Bornholm has recently set the national standard for enforcement. Since 2021, officials have systematically audited residency registers and, more importantly, utility usage patterns. By checking water and electricity consumption, authorities can identify "dark windows" that signify a speculative vacancy or an illegal short-term rental. On Bornholm alone, this crackdown reduced illegally empty year-round homes from 573 in 2023 to just 370 by late 2025.

For the resident, this is about community vitality. Kirsten Lund, a resident of Gudhjem, notes that neighborhoods like Nørresand now have "lights in the windows" throughout the winter—a direct result of the municipality forcing owners to either live in the homes or rent them out to permanent residents.

3. The Copenhagen Yield Paradox: Prestige Costs You Profit

For the sophisticated investor, central Copenhagen presents a "Yield Paradox." Data from 2026 reveals that the city’s most prestigious districts—Indre By, Frederiksberg C, and the sleek waterfront of Nordhavn—offer the lowest gross rental yields, typically compressing to between 2.5% and 3.3%.

Conversely, the "Yield Sweet Spots" are found in Nordvest and Valby, where gross yields approach 5%. This disparity is driven by a "Twin Speed" market. While property prices for flats surged by up to 20% through 2025—fueled by limited supply, "over-optimism," and steady in-migration—rents have hit a "mechanical compression" due to local affordability ceilings.

If you are hunting for income, look for the "Green Premium." Properties meeting EU taxonomy criteria for energy efficiency are now commanding rental premiums of 12-18% over older stock. Additionally, be wary of the andelsbolig (cooperative housing) structure. While prices are often lower than market value, these associations have strict resale rules and usage restrictions that can paralyze an investor’s exit strategy.

4. The Credit History Wall: 5% vs. 40% Down Payments

The Danish mortgage system is a global marvel, but for the expat, it is an impenetrable fortress. While a local buyer might secure a mortgage with a modest down payment, foreigners without a Danish credit history are frequently hit with a "risk premium" requirement of 20% to 40% down.

This "Credit Wall" reflects a broader national trend of financial caution. Even for local first-time buyers in the Capital Region, the typical down payment has risen from 5% in 2005 to 15% in 2024. For the newcomer, this capital requirement is compounded by hidden acquisition costs. Specifically, the tinglysningsafgift (registration fee) is DKK 1,850 plus 0.6% of the purchase price—or the official property valuation, whichever is higher. For properties with low purchase prices but high technical valuations, this can be an expensive surprise on closing day.

5. The "Sommerhus" Secret: A Forbidden Luxury

The most strictly guarded asset in the Kingdom is the sommerhus (holiday home). These coastal properties are legally protected to prevent foreign capital from pricing Danish citizens out of their own heritage. As a general rule, only Danish residents can purchase them.

This protectionism has created a staggering price gap that illustrates the power of the "Forbidden Luxury." In the picturesque town of Gudhjem, year-round homes trade for approximately 7,800 DKK per square meter. However, restricted summer houses in the same area hit 27,000 DKK per square meter. For the international buyer, the sommerhus is a coveted but legally elusive prize, requiring rare and specific dispensation from the Ministry of Justice that is seldom granted without a profound connection to the country.

Conclusion: Beyond the Brick and Mortar

The outlook for the Danish market remains bullish, with house prices forecast to rise by 4.5% in 2026. However, these gains are secondary to a more profound realization. In a market where the government can fine you 100,000 DKK for leaving a light off, buying real estate is an investment in a social contract.

The Danish system does not exist to maximize your IRR; it exists to ensure that towns like Nørresand remain living communities rather than seasonal ghost towns for offshore capital. As you navigate the bureaucratic "hygge" of the Ministry of Justice and the residency registers, you must ask yourself: is the Danish Dream worth the price of the social contract you are signing?

Written by

Under500K Team

Research and market insights for global property investors.