Discover how Brazil’s 2026 tax reform, 15% Selic rate, and new CIB registry are reshaping real estate, from Airbnb taxes to Golden Visa plays in secondary cities.

For decades, the global narrative around Brazilian real estate was one of informal charm: handshake rental agreements, "creative" tax exemptions, and a general lack of centralized oversight. To the uninitiated, the bureaucracy was a distant second to the beach view. Welcome to 2026. The handshake-and-Haver-view era has been superseded by a digital panopticon.

The landscape has fundamentally shifted into a highly regulated, transparent arena defined by a dual VAT system and a centralized digital eye. With the Selic interest rate holding steady at a restrictive 15% and the 2026 Tax Reform (Complementary Law No. 214/2025) now in full effect, the window for passive optimism has slammed shut. In its place is a sophisticated market where the "data-driven" investor is the only one left standing. For those who can navigate the new rules, these shifts aren't obstacles—they are the most significant buy signals in a decade.

The End of Informal Landlording: Meet the "CIB"

The era of "off the grid" rental income has officially ended with the launch of the Brazilian Real Estate Register (Cadastro Imobiliário Brasileiro – CIB). Think of the CIB as a "CPF for properties"—a single digital thread connecting land registries, the Federal Revenue Service, and individual bank accounts.

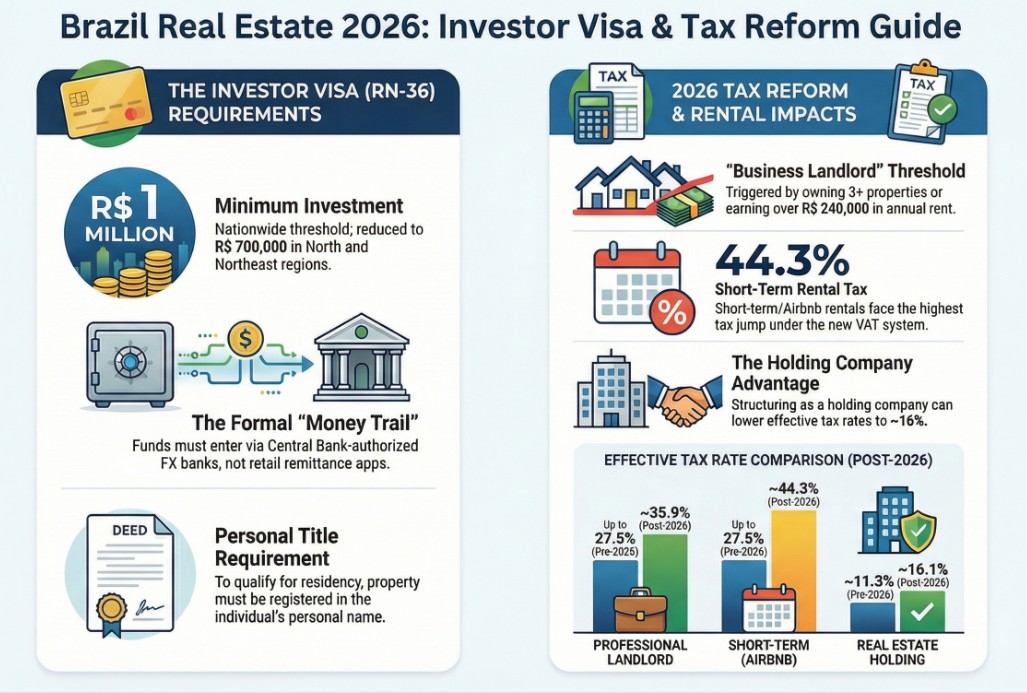

This transparency revolution automatically cross-references data from digital platforms like Airbnb and QuintoAndar with your tax returns and banking records. Crucially, the reform defines a "Professional Landlord" as anyone earning over R$ 240,000 annually from rentals or owning more than three properties. This threshold is not static; it is adjusted annually by the IPCA (inflation index), a vital nuance for long-term fiscal planning.

"Omissions will be easily detected, with fines of up to 150% of the unpaid tax plus interest. The age of informal or undeclared rentals in Brazil is coming to an end." — Oabitat

The Airbnb Tax Trap: Why Short-Term Rentals Just Got Expensive

If you are running a high-turnover short-term rental business, your ROI math likely changed overnight. Under the new dual VAT system (IBS/CBS), short-term rentals are now classified as a service, triggering a significantly higher tax burden than traditional leases.

While small, occasional landlords remain under standard IRPF brackets, professional activity is now heavily taxed. Individual landlords exceeding the R$ 240,000/3-property threshold face an effective tax rate of approximately 35.9%. However, for short-term vacation rentals, the total effective tax rate can soar to ~44.3%. This massive spike is driving sophisticated investors away from the "Airbnb hustle" and back toward professional management structures or traditional long-term leases, which remain more fiscally shielded.

The 15% Selic Paradox: Why High Rates are a "Cash Buyer’s" Best Friend

Standard economic logic suggests that high interest rates kill real estate. In 2026 Brazil, the 15% Selic rate—the highest in two decades—is actually a barrier that serves as a gift to the liquid investor.

High mortgage costs have effectively cleared the field of middle-market, mortgage-dependent competition. This has granted cash-ready buyers immense leverage, with negotiation discounts of 3% to 5% off asking prices becoming the norm in major hubs like São Paulo. The paradox deepens when you consider that while sales have slowed, rental demand is surging, with rents climbing 8–10% annually. This creates a "double-win" scenario: you secure the property at a discount while locking in gross yields of 6% to 7%—all while waiting for the inevitable rate-cutting cycle to trigger capital appreciation.

The "Northeast Discount": A Shortcut to the Golden Visa

For investors seeking residency, the RN-36 Real Estate Investor Visa (Brazil’s "Golden Visa") remains the premier route. While the national minimum investment is R 1 million, a strategic 30% reduction exists for those looking toward the North and Northeast regions, bringing the threshold down to R 700,000.

However, the strategist must mind the fine print: the investment must be in urban areas. The law explicitly excludes rural properties, and "rural" is defined strictly by taxation (paying ITR instead of the urban IPTU). Furthermore, the "money trail" is now a high-stakes compliance hurdle.

"Your funds must originate from outside Brazil and enter through the formal foreign exchange system... We strongly advise against using retail remittance apps... as they don't generate the Brazilian foreign exchange contract bank declaration tying your name and purpose to the transaction." — Luciano Oliveira, Oliveira Lawyers

The "Secondary City" Surge: Salvador and João Pessoa vs. The Big Two

The 2026 data shows a clear divergence. While the "Blue Chip" districts of São Paulo and Rio are seeing modest nominal growth of 5% to 7%, secondary markets are exploding. Salvador is leading the country, fueled by infrastructure projects like the Salvador-Itaparica Bridge.

*Growth driven significantly by Novo PAC infrastructure projects, including the Salvador-Itaparica Bridge.

From Individual to Institutional: The Rise of the Real Estate Holding

The single most important tactical pivot for 2026 is structural. If you meet the "Professional Landlord" criteria, remaining an "individual" owner is a fiscal error. The Tax Reform has made the Real Estate Holding Company the only viable path for wealth preservation.

Operating through a corporate structure (Lucro Presumido) allows for an effective tax rate of approximately 16.08%, a massive saving compared to the 44% faced by professional individuals. Furthermore, companies can claim IBS/CBS tax credits on maintenance, management fees, and even furniture—transforming what were once "cost centers" into structural tax efficiencies.

Conclusion: A Market for the Disciplined

The 2026 Brazilian market no longer rewards the amateur. We have transitioned from an era of passive optimism to one of data-driven precision. As the tax net closes on financial instruments—with a new 5% tax now applying to previously exempt assets like LCIs and FIIs—physical real estate has emerged as the final frontier of tangible asset protection.

Physical brick-and-mortar in Salvador or São Paulo represents a premier store of value and a hedge against the fiscal shifts of the new dual VAT era. The question for the 2026 investor is simple: Are your assets structured to thrive in the CIB era, or are you still trying to play by the rules of a Brazil that no longer exists? Success is no longer about finding the right beach; it’s about finding the right structure.

Written by

Under500K Team

Research and market insights for global property investors.