The German real estate market in 2026 has moved past the significant price corrections and volatility of recent years, entering a phase of gradual recovery and stabilization. The days of "free money" are over, and the market is finding a new equilibrium shaped by stabilized interest rates, chronic housing shortages, and massive regulatory shifts.

Here is a breakdown of the current status of the market:

-

Price Stabilization and Interest Rates After property prices corrected by 10% to 20% from their 2022 peaks, the downward slide has officially hit a floor in most major hubs. In cities like Berlin and Cologne, prices have already begun to creep back up. Mortgage interest rates have leveled off predictably between 3.0% and 4.0%, which has reduced buyer panic, killed off highly speculative competition, and improved negotiation leverage for those with solid capital.

-

Severe Supply and Demand Imbalance The single biggest driver of the 2026 market is the widening gap between population growth and available housing. The German government's goal of building 400,000 new homes annually remains unmet due to high construction material costs, developer hesitancy, and lengthy municipal permitting cycles. Because of this structural undersupply, vacancy rates in top-tier locations are near zero, which is driving rent prices up at record speeds and keeping residential real estate a dominant and resilient asset class.

-

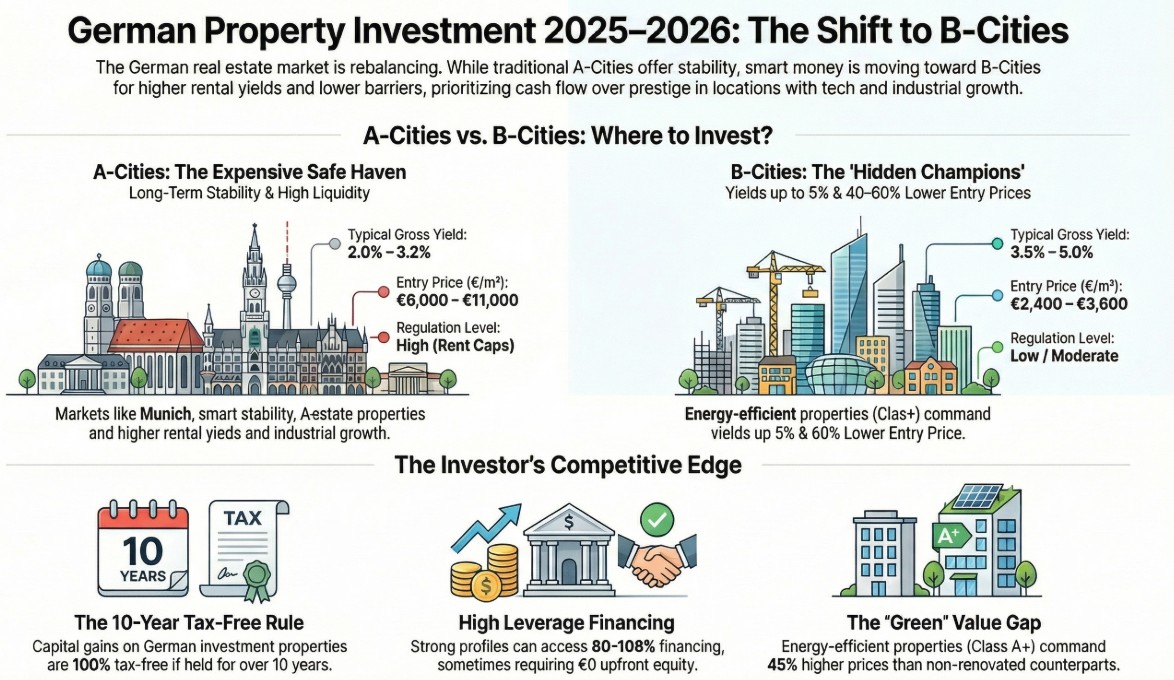

The Shift to "B-Cities" and Commuter Regions Investors are fundamentally shifting their geographic focus: A-Cities (Munich, Frankfurt, Berlin, Hamburg): These remain highly liquid and safe for capital preservation, but they are expensive, heavily regulated, and offer very low gross rental yields ranging from 2.0% to 3.5%. B-Cities and Peripheral Regions: Investors are increasingly pivoting to "B-cities" like Leipzig, Dresden, Nuremberg, and regional commuter hubs. These "hidden champions" offer lower entry prices (up to 40-60% cheaper than A-cities), less strict rent controls, and highly attractive rental yields between 3.5% and 5.5%.

-

The Green Transition and Energy Efficiency Energy efficiency has rapidly become just as important as location. To meet EU climate targets, more than 60% of Germany's current housing stock will need to be renovated by 2033. This has created a massive price divergence in the market based on energy labels. In 2026, unrenovated homes (Energy Label H) are seeing massive "renovation discounts," selling for an average of 45% less than highly efficient (Label A+) properties.

-

Landlord Regulations and Tax Reforms The market is navigating strict new regulatory frameworks: **Tenancy Law Reform (2026): **New laws have introduced a much tighter framework for landlords. This includes forced disclosures and limits on "furnishing surcharges," caps on index-linked rent increases (limited to 3.5% per year in tight markets), and heavy restrictions on consecutive short-term rentals to prevent landlords from bypassing rent controls. Tax Loophole Closures: The 2026-2027 era is seeing the dismantling of traditional real estate transfer tax (RETT) loopholes, such as the "share deal." The decoupling of RETT from the final title transfer and the expiration of partnership exemptions have forced massive internal reorganizations among institutional investors.

-

Boom in Niche Markets (Student Accommodation) Alternative real estate classes, particularly Purpose-Built Student Accommodation (PBSA), are thriving. Germany saw a record influx of 380,000 international students recently, leading to severe localized housing crunches. With high demand for furnished, flexible leases, the student accommodation market is expected to grow at a 10.4% CAGR to reach USD 4.73 Billion by 2031, drawing heavy institutional capital seeking inflation-linked, counter-cyclical cash flows.

Written by

Under500K Team

Research and market insights for global property investors.