Discover how Vietnam’s 2026 real estate market is shifting from speculative booms to state-led, value-driven growth, with new rules and infrastructure.

1. Introduction: The "Doi Moi 2.0" Ambition

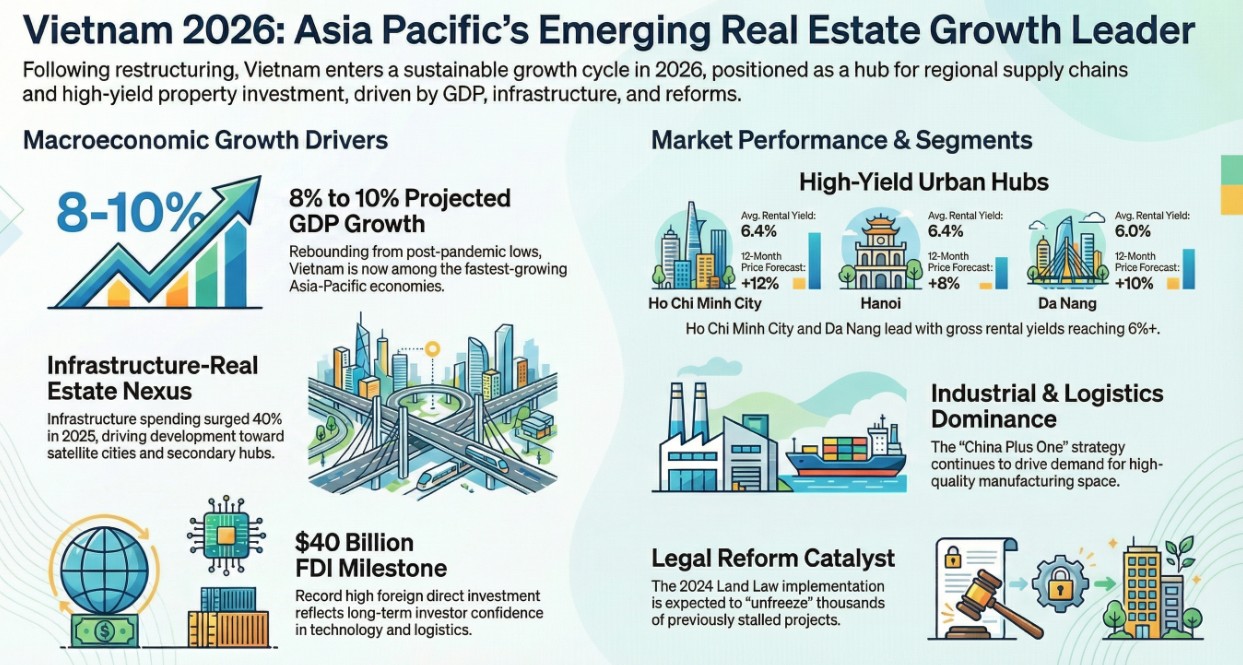

While the global economy settles into a period of "stable footing," Vietnam is aggressively pivot-shifting into what analysts are calling "Doi Moi 2.0"—a suite of structural reforms designed to propel the nation into high-income status. After a robust recovery through 2024 (7.1% GDP) and 2025 (8% GDP), the government has set a staggering 10% GDP growth target for 2026.

This is no longer a standard cyclical recovery; it is a fundamental re-engineering of the economy. For the strategic investor, the question is no longer about the existence of growth, but the nature of it. As the state moves to "unfreeze" the 80% of projects currently stalled by legal bottlenecks, 2026 will be defined by a transition from speculative fervor to a state-led, quality-driven market.

2. The Death of "Cheap": High-Value Growth Takes the Lead

Vietnam has officially outgrown its reputation as a low-cost assembly hub. Foreign Direct Investment (FDI) is now surging toward high-value-added sectors like AI-driven technology manufacturing and modern logistics. In Q1 2026, implemented FDI hit a five-year high of $5.41 billion, with manufacturing and processing commanding 82.8% of that total.

This shift demands a new class of industrial and residential infrastructure. As Neil MacGregor, CEO of Savills Vietnam, observes:

“Viet Nam has moved beyond the phase of attracting investment primarily based on cost advantages. Capital flows are now increasingly directed towards higher value-added sectors... This shift is reshaping real estate demand towards higher quality, sustainability, and longer-term development.”

3. The Infrastructure-Real Estate Nexus

To hit the 10% GDP target, the government is leaning heavily on three strategic levers:

- Consumption: Rebuilding household savings to fuel domestic retail (recovering to normal growth by mid-2026).

- Infrastructure: Scaling spending from 6% to 10% of GDP, following a 40% surge in 2025 and an anticipated 20–30% increase in 2026.

- Real Estate Development: Directly contributing 15% to GDP through both construction and indirect wealth effects.

The result is the rise of Transit-Oriented Development (TOD). With projects like the North-South Expressway and Long Thanh International Airport nearing key milestones, connectivity has replaced cheap credit as the primary driver of value. Investors are shifting focus toward satellite cities where infrastructure corridors create genuine "usage value" rather than speculative bubbles.

4. The Supply Paradox: Record Volume vs. The Selective Yield

The market is currently witnessing a massive supply surge. In 2025 alone, 128,000 new housing units were launched—an 88% increase from 2024 and the highest volume since 2019. However, this volume is profoundly skewed: 25% of new units are priced above VND 100 million per square meter, leaving affordable housing nearly absent from the primary market.

Strategic differentiation is now a requirement, as yields and risks vary wildly across the "Big Three" hubs:

- Ho Chi Minh City (Yield: 4.16%): High-risk profile due to oversupply, with 80% of new units concentrated in Thu Duc City.

- Hanoi (Yield: 3.54%): Strong fundamentals but witnessing price corrections as 18,454 new units hit the market.

- Da Nang (Yield: 6.0%): Medium-risk, benefiting from a 27% five-year price trend and a focus on beachfront luxury and suburban condos.

To correct this imbalance, the state has set a 2026 target of 160,000 social housing units, aiming to force "market-clearing prices" that end-users can actually afford.

5. 2026: The Year of the "State-Led" Market Principle

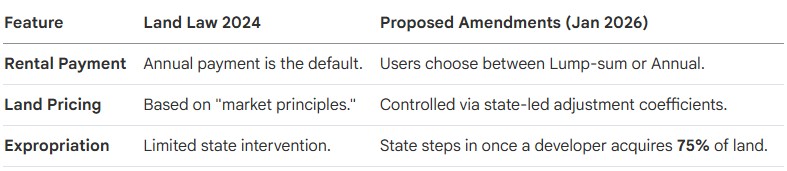

January 2026 marks a watershed moment in Vietnamese law. The government is moving away from pure "market principles" in land pricing (removing Article 158.1 of the 2024 Land Law) in favor of a more controlled, state-led framework to prevent price distortions.

Furthermore, the state is increasingly empowering "National Champions"—large conglomerates like Vingroup (VIC), whose family stocks now represent nearly 25% of the VN-Index. These champions are being tasked with leading infrastructure and project unfreezing, effectively sitting atop the development value chain.

This "75% rule" is the real rocket fuel for 2026; it allows the state to forcibly resolve the final 25% of land clearance bottlenecks, accelerating the "shovel-ready" status of thousands of stalled projects.

6. The $40 Billion Liquidity Tightrope

Despite the 10% growth ambition, investors must navigate a "Mosaic of Idiosyncrasies." The primary friction point is a $40 billion deposit shortfall in the banking system. In 2025, credit growth (19%) vastly outpaced deposit growth (15%), as savers chased gold (up 70%) and stocks.

The State Bank of Vietnam (SBV) is now performing a high-stakes balancing act:

- 1. Growth: Supporting the 10% GDP target through "informal QE" and balance sheet expansion.

- 2. Stability: Defending the VND against depreciation by guiding credit growth down to a more muted 15%.

For the real estate sector, this means developers with overpriced units or "low-provenance" legal status will face frozen conditions, while those aligned with state infrastructure goals will receive priority access to credit.

Conclusion: Selective Sustainability

2026 marks the end of the broad-based property boom. Vietnam is maturing into a cycle defined by "selective sustainability." As the nation transitions from a cost-driven to a value-driven economy, the winners will be those who move away from "flipping" toward the long-term management of high-quality, ESG-compliant assets. In this new era, the state is in the driver’s seat, and the road is paved with infrastructure.

Written by

Under500K Team

Research and market insights for global property investors.