Discover why Nordic real estate isn’t as simple as it looks in 2026, from Sweden’s cooperative ownership model to financing hurdles, ESG “transition alpha,” and high-yiel

The Nordic property markets have long enjoyed a global reputation for pristine transparency, institutional stability, and a "foreigner-friendly" regulatory environment. To the outside observer, Sweden, Norway, and Finland appear as the ultimate safe havens for international capital. However, as we navigate the complexities of 2026, fresh market data reveals a striking paradox: while the legal barriers for international buyers are virtually non-existent, the practical barriers—and the costs of misunderstanding them—have never been more punishing.

Even the most seasoned global investors are finding that these seemingly open markets are paved with structural nuances that can turn a high-prestige acquisition into a low-yield liability. Success in this region requires looking past the "face value" of a listing and dissecting the structural reality of the assets.

1. The Ownership "Illusion" – You Might Not Actually Own Your Apartment

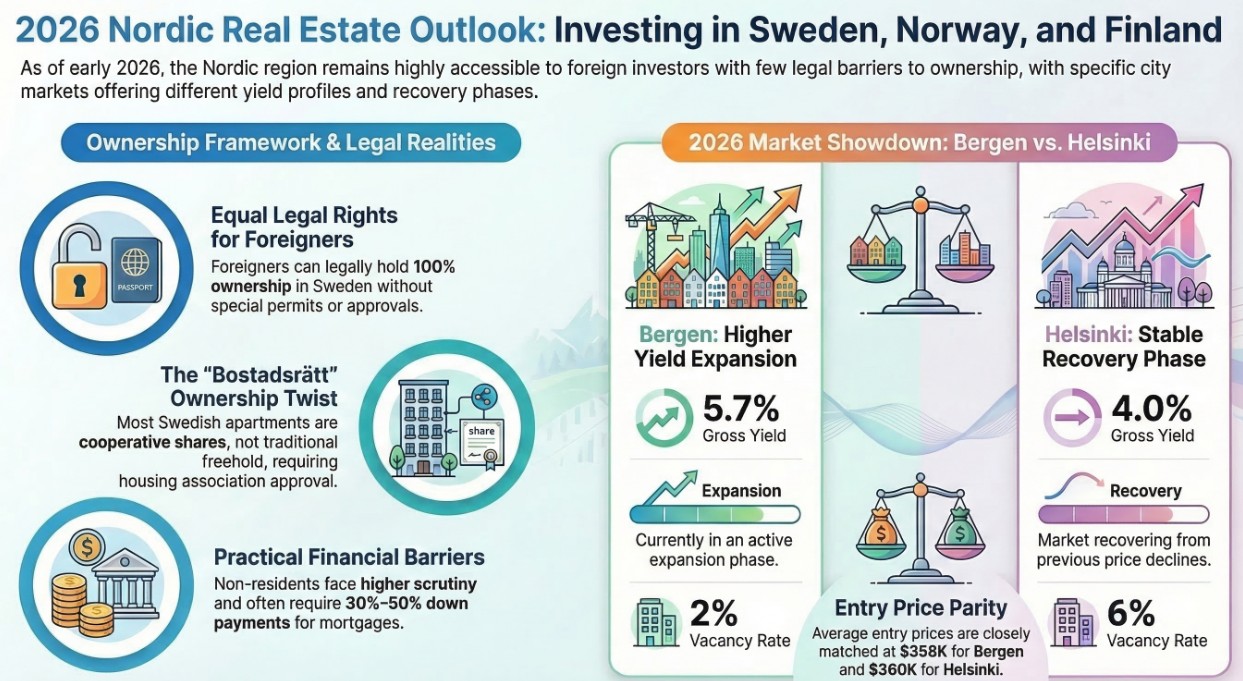

The most significant "twist" catching international buyers off guard in 2026 is the fundamental legal structure of apartment ownership, particularly in Sweden. Most buyers arrive expecting äganderätt (freehold ownership), which is the standard in most of the world and is the default for detached houses in the Nordics. However, the vast majority of the Swedish apartment market is built on the bostadsrätt model.

In a bostadsrätt arrangement, you do not own the physical unit or the real estate. Instead, you are purchasing a share in a housing cooperative (the Bostadsrättsförening or BRF), which grants you the right to occupy a specific unit. As the 2026 Investropa market data explicitly warns: "apartments are not owned as traditional real estate."

This is not a mere semantic difference; it is a fundamental shift in resident rights and investment liquidity. While ägandelägenhet (freehold apartments) exist, they remain a rare exception. In a BRF, your investment value is inextricably linked to the cooperative’s board decisions. The board has the power to reject prospective buyers, restrict subletting (often limiting your exit strategy or rental yield potential), and dictate the building's financial future.

2. The 15% "Expat Tax" – Why Foreigners Regularly Overpay

Analysis from early 2026 suggests that foreign buyers in Sweden tend to overpay by an estimated 5% to 15% compared to locals for comparable properties. On a 5 million SEK Stockholm apartment, this "misunderstanding premium" can reach 750,000 SEK.

This overpayment isn't a government levy; it is the result of a failure to analyze the capital structure of the housing association. While foreign investors frequently fixate on "apartment aesthetics" and location prestige, local buyers price their bids based on the BRF’s financial health. Locals scrutinize the "debt per square meter" and the interest rate sensitivity of the association’s collective loans.

If an association has high operating leverage or is facing a massive capex cycle for pipe replacements (stambyte), a local buyer will adjust their bid downward. A foreigner, seeing a renovated kitchen and a "safe" neighborhood, often pays a premium for an asset that carries a hidden share of the association's collective debt and the looming threat of rising monthly fees.

3. The Mortgage Wall for Non-Residents

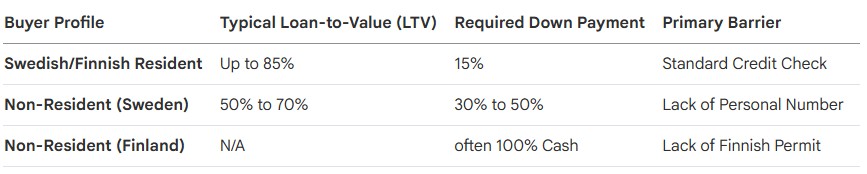

While no "legal restrictions" prohibit foreigners from purchasing property, the Nordic banking system has erected a formidable "practical barrier." Financing for residents versus non-residents is a tale of two markets.

The following table illustrates the financing gap as of 2026:

For non-residents, the lack of a "Personal Number" (or Coordination Number) is the ultimate hurdle. This number is the "master key" for the Nordic system; without it, you are functionally invisible to banks, utility providers, and insurance companies. In Helsinki specifically, non-EU/EEA investors often face a "no mortgage access" reality without a Finnish permit, forcing them into cash-only transactions that severely limit leveraged returns.

4. Sustainability as "Transition Alpha"

The Nordic market is currently the primary testing ground for the EU Taxonomy, and smart capital is moving away from simply buying "dark-green" assets. Instead, the focus has shifted to "Transition Alpha."

Using data from DNB’s ESG Insight, we can identify "transition enablers"—companies like JM AB and Catena AB. These entities are standing out because their sustainable capex is higher than their current sustainable revenue. This is the literal alpha signal: these companies are aggressively "greening" their infrastructure before those assets are fully priced as sustainable by the broader market.

For the 2026 investor, the alpha is found in the direction of the transition. These institutional standards are rapidly becoming the valuation floor for individual apartment associations as well. A BRF that fails to transition its heating and energy infrastructure today will see its valuation decimated by 2030.

5. The Yields Are in the Periphery

While city centers in Stockholm and Helsinki offer "trophy" stability, the most compelling yields are found in suburban "high-yield" areas. 2026 data highlights two specific opportunities for investors who can bypass financing barriers with cash:

- Bergen, Norway: While the center is saturated, periphery districts like Åsane and Fyllingsdalen are delivering gross yields of 5.8% to 6% on units under $500,000. The catalyst here is the Bybanen light rail extension, which is fundamentally altering commuter dynamics and boosting value in these formerly overlooked zones.

- Helsinki, Finland: The market is in a "recovery phase," with prices in certain suburbs stabilizing at attractive entry points. Specifically, Malmi (averaging €4,100/sqm) and Kontula (averaging €3,800/sqm) are offering yields above 5%. These areas represent the best value-for-money for cash-rich investors who can weather the current lack of residential financing.

Conclusion: Moving Toward the 2030 Horizon

The Nordic markets remain some of the most secure in the world, with Corruption Perception Index (CPI) scores between 81 and 87. This signals a high level of rule-of-law, but security should not be mistaken for simplicity. The system will not cheat you, but its structure might—if you do not understand it.

As we look toward 2030, the successful international investor will be the one who looks past the "foreigner-friendly" label to dissect the underlying cooperative debts, the ESG transition metrics, and the infrastructure-led shifts in peripheral yields.

In your next investment, will you prioritize the property’s "face value" or its "structural reality"? The answer will determine whether you are part of the 40% of foreigners who feel friction in this market, or the small percentage who truly master it.

Written by

Under500K Team

Research and market insights for global property investors.