Torn between NYC and Jersey City in 2026? Discover seven surprising truths about co-ops, Mansion Tax cliffs, Jersey City yields, and how to save $200K in interest.

The $200,000 Secret: 7 Surprising Realities of Navigating the 2026 Tri-State Property Market

As we move into 2026, the Tri-State real estate market is defined by what analysts call a "Real Estate Fog"—a dense mix of interest-rate volatility, tariff uncertainty, and shifting migration patterns. While some see this as a reason for caution, sophisticated investors recognize it as a period of profound structural opportunity. The "buy" rating for the U.S. market is currently at a 20-year peak precisely because liquidity often hides where others see only uncertainty.

To navigate this landscape, one must move beyond the macro-headlines and master the micro-level nuances of the urban grid. From the legal quirks of Manhattan ownership to the infrastructure-driven boom in Jersey City, these seven realities represent the current playbook for building equity in the nation’s most competitive corridor.

1. The Ownership Illusion: Why Your NYC Co-op Isn’t Actually "Real Estate"

In New York City, the most common path to "ownership" doesn’t involve a deed. Co-ops, which comprise the vast majority of Manhattan’s housing stock, are legally classified as "personal property" rather than "real property." When you buy a co-op, you are purchasing shares in a corporation; in exchange, you receive a proprietary lease. This distinction is the primary reason co-ops are typically 20% to 30% cheaper than condos.

For the strategic buyer, this legal structure offers a massive upfront financial advantage. Because you are not purchasing "real property," you are exempt from title insurance requirements and NYC’s significant mortgage recording tax. However, the trade-off is board rigidity. Expect a minimum 20% down payment and a rigorous "neighbor vetting" interview. You are essentially trading your freedom to sublet or renovate for the financial stability and exclusivity of a corporation.

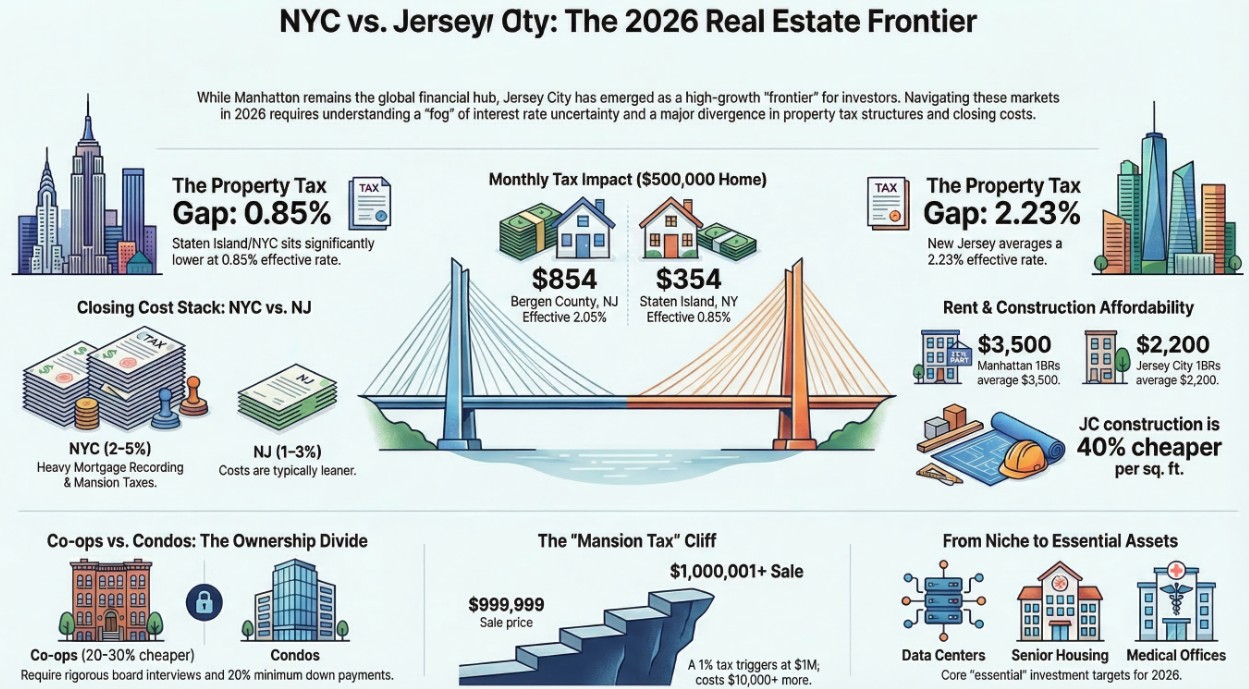

2. The $1 Cliff: How a Single Dollar Can Cost You $10,000 at Closing

The NYC "Mansion Tax" remains one of the most punitive cliff taxes in the country. It is a 1% residential tax that applies to the entire purchase price the moment a sale hits $1,000,000. Because there is no gradual phase-in, the difference between a $999,999 sale and a $1,000,001 sale is a five-figure penalty.

"A property sold for $999,999 has $0 mansion tax, but a property sold for $1,000,001 costs you an extra $10,000+ at closing."

This reality has made $999,999 a strategic ceiling for sellers and a target for value-seeking buyers. While the tax scales up to 3.9% for properties over $25 million, the one-million-dollar threshold is where most first-time buyers feel the sting. Mastering this "cliff" is essential for effective negotiation and accurate closing-cost budgeting.

3. The 15-Year "Magic Number" for NYC Equity

The true "secret" to building massive equity in the Tri-State area isn't found in a hot neighborhood, but in your amortization schedule. While the 30-year fixed-rate mortgage offers lower monthly payments for NYC’s high cost of living, the 15-year fixed-rate mortgage offers "rock-bottom" rates that represent a much lower risk to lenders. On a typical NYC apartment, choosing the shorter term can save a buyer more than $200,000 in total interest over the life of the loan.

15-Year Benefit Data: By choosing a 15-year term over a 30-year term, a buyer builds "real" ownership twice as fast and saves a staggering $200,000+ in interest—essentially the cost of a luxury renovation.

For many sophisticated owners, the ultimate "NYC Strategy" is a wealth management pro-tip: secure a 30-year mortgage to maintain monthly budget flexibility, but use annual bonuses to make extra principal payments. This allows you the safety of a lower required payment while effectively paying down the loan like a 15-year mortgage, securing that $200,000 in interest savings without the rigid monthly commitment.

4. From "Niche" to "Essential": The Data Center and Self-Storage Takeover

The investment landscape has fundamentally shifted since the pre-Great Recession era. In 2006, analysts noted that "investors will continue to scavenge for opportunities in more niche property categories... as long as core categories seem overpriced." Twenty years later, those "niches" have become the essential infrastructure of the modern economy. Data centers and self-storage are no longer side-bets; they are core holdings that often outperform traditional office and retail.

Data centers, in particular, are seeing a "tremendous amount of capital" due to the rapid adoption of generative AI and the digitization of the economy. These aren't just buildings; they are powered infrastructure. This transition represents a shift from speculative real estate to essential services, reflecting a broader social and energy transition.

"Data center, digital infrastructure... those are true infrastructure investment... providing an essential service. Anything essential services, doesn’t matter if it’s a physical, social, or energy transition."

5. The "Sponsor" Penalty: The Hidden Cost of Buying Brand New

In NYC, buying a brand-new "Sponsor unit" directly from a developer is the most expensive way to close. Custom dictates that when you buy new construction, the buyer shoulders the taxes and fees that the seller traditionally pays in a resale. This "Sponsor Penalty" can push your closing costs to a staggering 5% or 6% of the purchase price.

Beyond transfer taxes, buyers are expected to pay for the Sponsor’s attorney (typically 2,500–3,500) and a pro-rata share of the Resident Manager’s unit (often 3,000–10,000+). Most critically, buyers must contribute 1–2 months of common charges to a "Working Capital Fund" to seed the building’s bank account. These "hidden" costs mean that a "pristine" unit carries a much higher entry price than the sticker suggests.

6. The "VIP Seat" Advantage: Why Jersey City is the Smart Manhattan Alternative

Jersey City has transitioned from a Manhattan alternative to a primary destination for smart capital. Analysts call this the "VIP Seat" advantage—offering unparalleled views of the Manhattan skyline at a fraction of the cost. With PATH connectivity providing a 10-to-25-minute commute to Wall Street or Midtown, the distance is often shorter than traveling from Upper Manhattan or deep Brooklyn.

The financial disparity remains the primary driver of this trend. While Manhattan rents average $3,500, Jersey City offers comparable luxury at $2,200. This rent gap is supported by a significant construction cost advantage that allows developers more room for modern amenities.

- Average Construction Cost per Square Foot:

- Manhattan: 600–700

- Jersey City: 300–400

7. Navigating the 2026 "Fog": Uncertainty as an Investment Strategy

The current market is defined by "Real Estate Fog"—a mix of tariff-induced construction cost spikes and migration uncertainty. However, this period of market dislocation is exactly why the "buy" rating is at a 20-year peak. Sophisticated investors aren't waiting for the fog to clear; they are deploying "dry powder" now to avoid the cap rate compression that will inevitably follow when interest rates stabilize.

Whether you view the fog as "heavy" or "patchy," the strategy for 2026 is one of granular asset selection. Success no longer comes from broad macro-bets, but from finding liquidity in subsectors with durable demand, such as medical offices or AI-driven digital infrastructure. This is a "back to basics" cycle where operational excellence and income growth matter more than simple market appreciation.

"Today’s market does not reflect where we are going."

Conclusion: The Future of the Urban Grid

As the Tri-State market evolves, the era of "stable" macro-trends has been replaced by a tech-enabled, micro-driven reality. Success in 2026 requires looking past the skyscrapers of today to identify the essential services of tomorrow. The question for every participant in this market is no longer just about location, but about timing and adaptability.

Are you chasing the perceived stability of the Manhattan of today, or are you positioned to capture the high-yield liquidity of the next decade's essential sectors? In this fog, the greatest risk isn't the uncertainty—it's the hesitation to move while others are waiting for the sun to rise.

Written by

Under500K Team

Research and market insights for global property investors.